Community Bank Strategy: The Value Equation

Most community bank CEOs believe performance determines value.

Strong earnings.

Disciplined credit.

Consistent growth.

Efficient operations.

And performance does matter.

But performance alone does not create premium value.

Two institutions can look nearly identical on a spreadsheet — yet experience very different outcomes when evaluated.

The difference is not performance.

It is transferability.

The Hidden Variable in Community Bank Valuation

Over time, a simple equation becomes clear:

Performance × Transferability = Premium Value

Most institutions focus heavily on the first variable.

Very few deliberately build the second.

Performance answers one question:

How well are we operating today?

Transferability answers a different one:

Will this performance survive change?

That distinction is subtle.

And it is where leverage is either built — or quietly eroded.

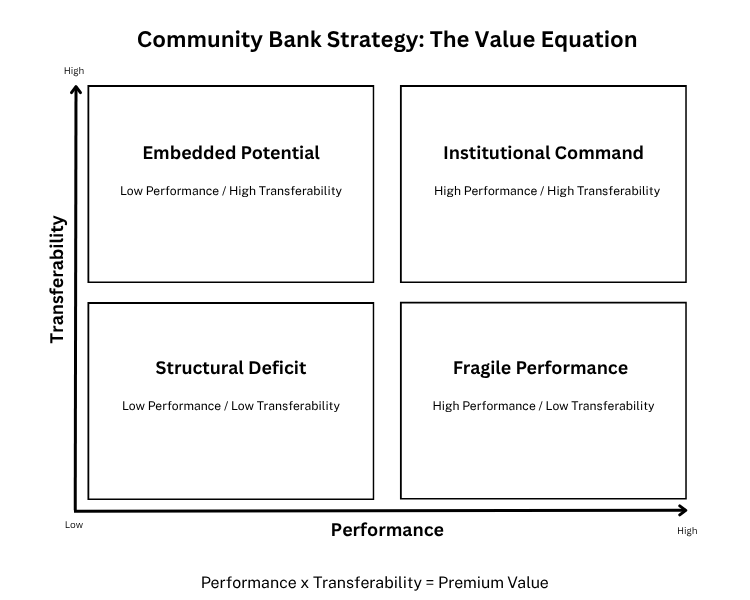

The Value Equation Matrix

To make this practical, consider a simple two-by-two framework:

- Horizontal axis: Performance (Low → High)

- Vertical axis: Transferability (Low → High)

This produces four structural positions.

1) Structural Deficit

Low Performance / Low Transferability

The weakness is visible.

The risk is obvious.

Performance is inconsistent, and the institution lacks structural depth.

These banks are rarely surprised by compressed outcomes — because fragility is already apparent.

2) Fragile Performance

High Performance / Low Transferability

This is where many strong banks quietly sit.

The numbers look impressive.

But the performance is concentrated.

It lives inside individuals — not inside the institution.

A dominant CEO.

A handful of key lenders.

A concentrated depositor base.

Institutional knowledge that is undocumented.

If leadership changes, the results may change too.

The performance is real.

But it is fragile.

And sophisticated buyers discount fragility.

3) Embedded Potential

Moderate Performance / High Transferability

The earnings may not be extraordinary.

But the structure is sound.

Leadership depth exists.

Customer relationships belong to the institution.

Systems are scalable.

Governance is aligned.

Buyers see durability.

And durability creates optionality.

These institutions often command stronger outcomes than their performance alone would suggest.

4) Institutional Command

High Performance / High Transferability

This is where premium value begins to appear.

Performance is strong.

And the structure ensures it survives transition.

Results belong to the institution — not to one executive, one lender, or one relationship.

The future can withstand change.

And the market pays for that confidence.

Why Performance Alone Doesn’t Command Premium

In community banking, performance gets you into the conversation.

Transferability determines whether you command a premium.

Premium is not a multiple.

Premium is durability.

Premium is optionality.

Premium is structural resilience.

Two banks can report similar ROA, capital ratios, and growth metrics.

Yet one may receive an ordinary price.

The other may receive a significant premium.

The spreadsheet does not explain the difference.

Structure does.

The Transferability Gap

There is a quiet gap inside many institutions.

Not a performance gap.

A transferability gap.

Performance is measured quarterly.

Transferability is rarely measured with the same rigor.

Consider two banks of similar size and earnings.

In one:

Succession has been discussed calmly — long before urgency.

Leadership depth has been intentionally built.

Board philosophy is aligned.

Capital optionality exists.

Strategic identity is clearly defined.

In the other:

Performance is strong.

But depth depends quietly on one or two individuals.

Conversations are postponed.

Alignment is assumed.

Drift is tolerated.

On paper, they are indistinguishable.

Under scrutiny, they are not.

Both perform.

Only one is deeply transferable.

That difference does not show up first in earnings.

It shows up in fragility.

And fragility compresses leverage.

Why This Matters Even If You Never Sell

Understanding transferability does not signal intent.

It signals stewardship.

Most banks that deliberately strengthen transferability never pursue a transaction.

But readiness changes outcomes — whether a transaction occurs or not.

It influences:

Board confidence

Shareholder communication

Succession planning

Capital strategy

Negotiation posture

Cultural stability

Transferability is not a transaction strategy.

It is institutional hygiene.

And hygiene protects leverage long before leverage is tested.

The Question That Follows

Once you understand the Value Equation, the diagnostic question changes.

Instead of asking:

“How are we performing?”

You begin asking:

“If leadership changed tomorrow, how much of our performance would remain?”

And more importantly:

“What, exactly, would break?”

Those questions are uncomfortable.

But they are clarifying.

Because the goal is not performance alone.

The goal is performance that survives transition.

That is what commands premium value.

That is what preserves optionality.

And that is what builds control — long before anyone asks the question.

For leaders who want to explore how performance and transferability are evaluated in real institutional settings, the Community Bank Value™ Strategic Briefing examines these structural drivers in greater depth.

It is not a transaction discussion.

It is a strategic clarity session.

You can learn more here:

Community Bank Strategy: Why Control Is Built Before It’s Tested

This framework is explored further in The Value Equation episode of the Community Bank Value™ Playbook for those who prefer to engage with it in audio form.

Categories

All Categories a bank ceo's step-by-step guide account management accountability acknowledgment acquisition costs acquisition planning acquisition readiness acquisition risk acquisition strategy acquisition success acquisition target acquisition targeting advisory board annual business planning annual meeting annual meeting strategy annual meetings asset size assumption examination auction process authority transition balance sheet management balance sheet optimization balancing act bank acquisition bank capacity bank ceo bank ceos bank culture bank directors bank examination cycle bank exit planning bank exit strategy bank financials bank leadership bank m&a bank m&a strategy bank management bank merger bank mergers bank multiples bank operations bank performance bank profitability bank sale negotiation bank sale preparation bank sale process bank sale strategy bank scale bank shareholder value bank story bank strategy bank succession planning bank valuation bank valuations bank value banking banking culture banking economics banking leadership banking relationships banking scale baseball analogy behavioral incentives benefits communication board alignment board and shareholder alignment board approval board culture board decision making board documentation board dynamics board education board effectiveness board expertise board governance board management board meeting board meetings board members board of directors board preparation board recognition board recommendation board relations board relationships bond portfolio management bonus structure book vale dilution borrower relationships brand inventory brand transition business continuity business development business model evaluation business preparation business psychology buyer evaluation buyer identification buyer interest buyer meetings buyer outreach buyer perspective buyer pool development buyer presentation buyer questions buyer relations buyer relationships buyer research buyer screening buyer types buyer's perspective buyer-ready bylaws review calling blitz capacity assessment capital allocation capital constraints capital flexibility capital management capital planning capital policy capital strategy career advancement career development career pathing career reflection career transition cash vs stock cash vs stock offers ceo disengagement ceo leadership ceo mindset ceo preparation ceo role ceo transition certainty of closing certificate surrender change management change-in-control agreements client briefings closing checklist closing day commecial lending commercial lending commmunity banking communication strategy communication systems community bank community bank ceo community bank merger community bank strategy community banking community bankng comparable transactions compensation design competitive advantage competitive analysis competitive bias competitive bidding competitive intelligence competitive positioning competitive response competitive threats competitor analysis competitve recruiting complementary acquisition confidential information memorandum confidential process confidentiality confidentiality agreements confidentiality management confidentiality protection consensus building consistency vs. performance consistent performance constraint accepted continuity planning contract management contract negotiation contract obligations contract terms control assessment control dynamics core earnings core processing core processing contract core system migration corporate administration corporate communications corporate culture corporate documents corporate governance cost structure analysis cost synergies covid impact credit concentration credit culture credit demand credit policy credit quality credit trends credit union acquisitions culteral consistency cultural assessment cultural compatibility cultural fit cultural fit concerns cultural keeper cultural knowledge cultural sensitivity cultural transition cultutral fit customer anxiety customer communication customer dependency customer diversification customer experience customer influence customer information customer loyalty customer relationships customer retention customer satisfaction customer service customer trust customers d&o insurnace data management data room management deal announcement deal closing deal comparison deal completion deal confidentiality deal control deal evaluation deal execution deal fatigue deal lawyers deal leverage deal management deal positioning deal process deal protection deal risk deal structure deal structuring deal team deal terms deal timeline deal-killers decision authority decision concentration decision framework decision gravity decision making decision posture decision quality decision-making bias decision-making independence decision-making process deconversion costs defensive posturing definitive agreement delegation delegation skills deliberate decisions deposit behavior deposit diversification deposit growth deposit mix desposit stability diagnostic framework digital transformation director engagement director influence director liability discounted cash flow discretion management diversification dividend policy dividend strategy document management due diligence due diligence preparation duty of care duty of loyalty early termination fees earnings durability earnings impact earnings quality earnings sustainability efficiency ratio electronic delivery embedded potential emotional intelligence emotional preparation employee appreciation employee benefits employee communication employee development employee engagement employee management employee morale employee motivation employee protection employee respect employee retention employee transformation employer branding engagement strategy environmental inspections equity investment established approaches executive compensation executive engagement executive leadership executive transition exit planning exit planning for banks exit stages exit strategy expense management experience dependency face-to-face meetings fairness opinion familiar patterns family-owned banks faq development fdic data federal home loan bank fee generation fee income growth fee income oppotunities fee income streams fee structure fiduciary duty fiduciary responsibility final negotiations financial anaiysis financial analysis financial performance financial planning financial projections financial reporting first impressions formal deliberation forward-thinking leadership fragile performance franchise value funding costs future acquirers future leaders future planning future potential general counsel generational shifts generational workforce geographic expansion geographic footprint golden window good faith governance clarity governance effectiveness governance structure gratitude perspective growth narrative growth opportunities growth paths growth potential growth strategy growth targets growth trajectory growth vs. discipline herd mentality hidden value how to sell a bank how to sell your bank human resources implicit understanding incentive structure incentive structures independence independent directors independent thinking individual dependency inflection points informal process informal standards information control information leaks information security inherited assumptions initial offers innovation resistance insider agreements insitutional control institutional authority institutional balance institutional command institutional control institutional culture institutional direction institutional durability institutional dynamics institutional fragility institutional hygiene institutional knowledge institutional preparedness institutional priorities institutional resilience institutional reslience institutional strength institutional structure institutional weight integration planning integration timeline interview techniques intrinsic value investment banker role investment banker selection investment bankers investment banking ipo (initial public offering) irs 280-g rules key employees key personnel knowledge management knowledge portability knowledge transfer kurt knutson leadership alignment leadership assessment leadership bench leadership centralization leadership change leadership communication leadership confidence leadership dependency leadership depth leadership development leadership distribution leadership grace leadership gratitude leadership hesitation leadership independence leadership legacy leadership philosophy leadership pipeline leadership strategy leadership styles leadership transition leadership transitioon legacy brand legacy building legal agreements legal counsel legal documentation legal expertise legal fees legal representation legal responsibilities lending limits letter of intent letter of intent (loi) letter of transmittal leverage leverage building leverage matrix lifecycle management liquidity event loan growth loan participations loan portfolio loan portfolio management loan-to-deposit ratio long-term planning long-term resilience long-term value m&a (mergers & acquisitions) m&a process m&a readiness m&a strategy management assessment management depth management development management independence management meetings management philosophy management succession management team margin management market competition market conditions market cycles market demographics market differentiation market education market intelligence market opportunity market position market positioning market research market specialists market strategy market testing market timing market valuation market value material adverse change maximizing deal value media relations meeting follow-up meeting preparation meeting strategy meeting structure mental health mental hurdles mental preparation merger agreement merger agreements merger consideration merger economics merger integration merger mindset merger of equals mergers & acquisitions (m&a) message coordination midyear assessment midyear review milestone recognition minimum price multi-genrational banks multiple approach valuation negotiating leverage negotiation leverage negotiation preparation negotiation strategy net present value neutral advisory next chapter planning niche strategy non-binding offers non-compete agreements non-core earnings non-disclosure agreements objective analysis ocassional acquirers offer analysis offer comparision offer evaluation one-buyer approach one-on-one meetings operating independence operational assistance operational consistency operational constraints operational decisions operational efficiency operational flexibility operational independence opportunity assessment optionality organizational architecture organizational behavior organizational change organizational clarity organizational comfort organizational consistency organizational culture organizational development organizational drift organizational evolution organizational excellence organizational flexibility organizational identity organizational inertia organizational memory organizational resilience ownership concentration ownership structure past vs. future focus pattern recognition paying agent payment processing per-share value performance assessment performance expectations performance managemnt performance metrics performance optimization performance stability perfromance continuity perfromance metrics personal fulfillment personal growth physical signage planning cycle planning discipline planning preparation policy development policy interpretation portfolio analysis portfolio diversification portfolio management position assessment position before pressure post-announcement period post-closing celebration post-closing integration post-closing period post-closing process post-closing strategy post-loi management post-merger integration post-sale planning post-sale role power dynamics power shift pre-emptive strategy pre-meeting alignment predictability premium buyers presentation skills press release price negotiation price-to-book multiples priority communication private decision-making proactive planning process control process documentation process formalization process management process transparency professional communication professional development professional growth professional guidance professional identity professional leadership professional presentation professional representation professional reputation professional responsibility protective instincts proxy materials psychological traps public communication reactive strategy readiness assessment real estate surveys recruitment strategy recurring revenue regulatory approval regulatory burden regulatory compliance relational gravity relationship banking relationship buiding relationship building relationship management relationship risk relationship weight reputation risk resource management responsibility shift retention strategy return on assets (roa) return on investment revenue producers reverse engineering reward systems risk absorption risk assessment risk aversion risk management risk mitigation risk tolerance roi analysis role adjustment role profiling role profilinig role transition rural banking sale preparation sale strategy sale timing sale-ready sales process sales strategy savvy banker strategies scalable oprations scale advantage scarcity mindset sell your bank sell-side advisory seller psychology seller types seller's mindset selling on your terms selling your bank senior leadership serial acquirers share conversion shareholder alignment shareholder analysis shareholder approval shareholder communication shareholder data shareholder expectations shareholder legacy shareholder meeting shareholder payment shareholder protection shareholder records shareholder relations shareholder return shareholder returns shareholder rights shareholder value shareholders short-term performance silent running perios (pre loi) social media management sop development special meeting stakeholder management status quo bias stay-put agreements stock certificates stock transfer agent strategic alignment strategic alternatives strategic architecture strategic asset strategic caution strategic clarity strategic command strategic communications strategic constraints strategic control strategic decision making strategic direction strategic distance strategic erosion strategic fit strategic fit analysis strategic flexibility strategic framework strategic governance strategic growth strategic hiring strategic isolation strategic leadership strategic leverage strategic maneuvering strategic optionality strategic options strategic partnerships strategic perspective strategic planners strategic planning strategic position strategic positioning strategic process strategic research strategic stewardship strategic thinking strategic timing strategic value strategic value creation strategic vision strategic vulnerability strategic window stress management structural clarity structural deficit structural durability structural fragility structural messaging structural readiness structural resilience structural reslience structural strength succession planning succession strategy surplus mindset sustainable growth system conversion system thinking systems and processes systems architecture systems discipline systems thinking tacit knowledge talent acquisition talent assessment talent development talent identification talent management talent protection talent retention talent scarcity talent succession planning tanible book value (tbv) team autonomy team building team confidence team continuity team independence team preparation team recognition technology capabilities technology integration tempo management the art of selling your bank third-party contracts three-step plan time management timeline planning track record training development transaction analysis transaction approval transaction attorneys transaction complettion transaction conditions transaction costs transaction execution transaction management transaction process transaction security transaction timeline transaction timing transferability transition management transition risk treasury management unique value proposition urban banking valuation methodology valuation methods valuations value assessment value creation value drivers value enhancement value equation value maximization value optimization value proposition value-based strategy variation absorption vendor management virtual data room voting process voting rights wealth management websire migration weekly reporting work-life balance workforce planning written offers